Is an ILP Better Than Investing Directly in the S&P 500?

With more options available to retail investors, more NRIs are engaging with the stock market than ever. However, not all investors know how to create wealth using these tools. The most common purchases that retail investors make are either the S&P 500 or a similar ETF such as VTI or VOO. While these are excellent entry points to learn how to invest and build a savings habit, it might not be the best strategy for long-term investors hoping to use the gains from their portfolio to retire. This blog post will explore exactly why investing in the S&P 500 might not reap the rewards that you expect in 2026 and beyond.

What Is the S&P 500?

The vast majority of NRIs have heard about the S&P 500. If you haven’t, that’s fine, we don’t judge here. The S&P 500 is a stock market index that tracks the performance of 500 of the largest publicly traded companies in the United States, providing a broad snapshot of how the U.S. stock market and economy are performing.

The companies in the index come from many industries and are weighted by market capitalization, meaning larger companies have a bigger impact on the index’s movement. Because it includes major firms such as Apple, Microsoft, and Amazon, investors often use the S&P 500 as a key benchmark to measure investment performance and the overall health of large U.S. companies.

5 Reasons the S&P 500 Is Not the Holy Grail of Investing for NRIs

1. Lack of Global Diversification

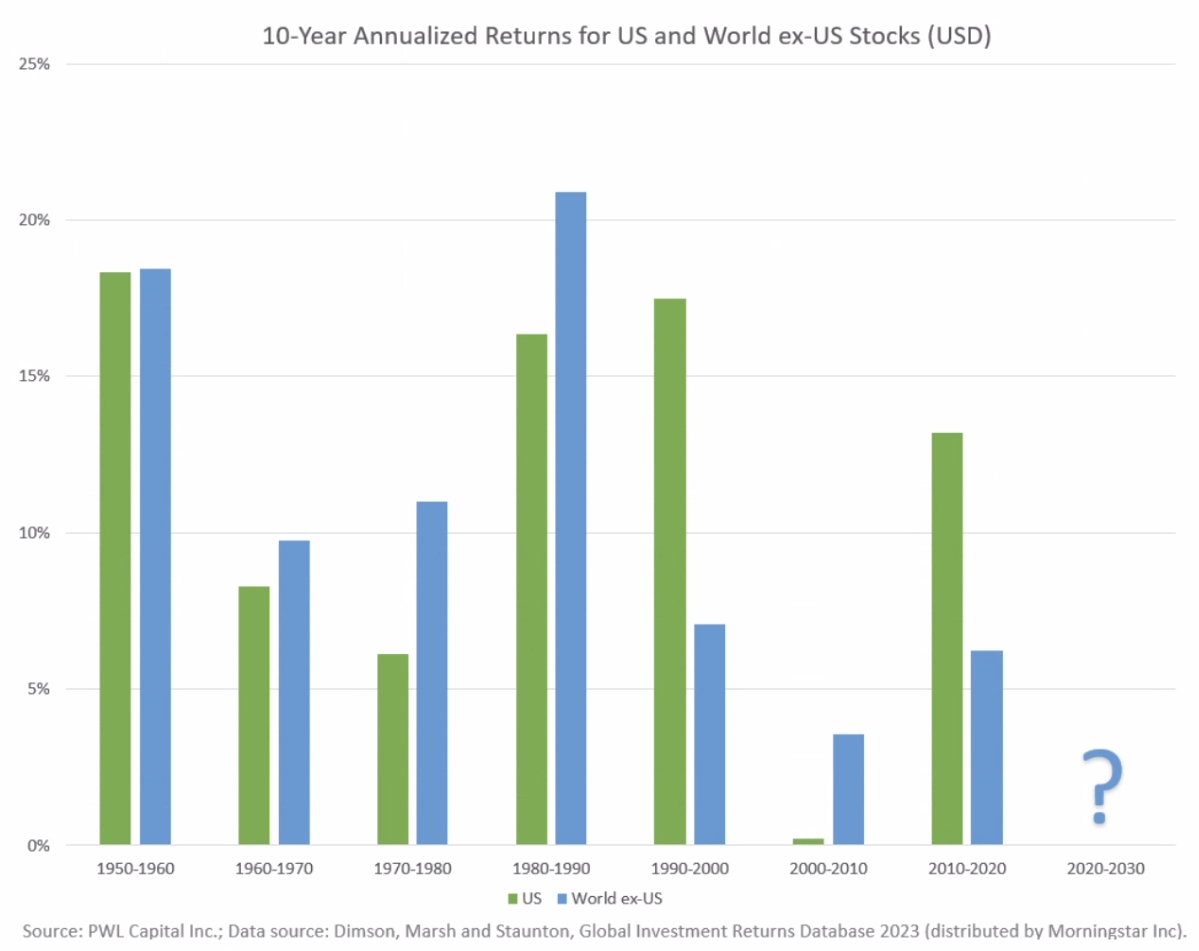

One of the biggest limitations of investing exclusively in the S&P 500 is the lack of global diversification. Although the companies in the index operate internationally, the index itself represents only U.S.-listed companies. This means investors are heavily exposed to a single market and a single economy.

Global economic growth does not occur evenly. At different points in time, other regions such as Europe or emerging markets may outperform the United States. Investors who concentrate their entire portfolio in a single market risk missing out on growth opportunities elsewhere in the world. A diversified global portfolio can help spread risk and capture opportunities across multiple economies rather than relying on just one.

Performance of US stocks against the rest of the world’s stocks

2. Heavy Concentration in a Few Mega-Cap Stocks

Another concern with the S&P 500 is its increasing concentration in a handful of mega-cap technology companies. Because the index is weighted by market capitalization, the largest companies have a disproportionate influence on the index’s performance.

For example, companies such as Apple, Microsoft, Amazon, NVIDIA, and Alphabet now make up a significant portion of the index. This means that the performance of the S&P 500 is increasingly tied to the fortunes of a small number of companies. If these firms experience slower growth or market corrections, the overall index may be significantly affected.

3. Massive Sector Concentration Risk

Closely related to stock concentration is sector concentration risk. Over the past decade, technology companies have grown rapidly and now dominate the S&P 500. While this has boosted returns during strong tech cycles, it also creates vulnerability if the technology sector experiences a downturn.

Markets historically move in cycles, with different sectors outperforming at different times. A portfolio that is heavily weighted toward a single sector may struggle during periods when that sector underperforms. Diversifying across industries such as healthcare, energy, financials, and consumer goods can help reduce this type of risk and provide more balanced growth over time.

4. Hidden Tax Implications for Non-US Residents

Tax considerations are another important factor for NRIs investing directly in U.S. markets. Non-U.S. residents may face withholding taxes on dividends from U.S. stocks and ETFs. Since neither Singapore nor India has a tax agreement with the U.S., any dividends that you receive from the S&P 500 are subject to a 30% withholding tax.

In addition, U.S. estate taxes can apply to certain assets held by non-resident investors, potentially creating complications for long-term wealth planning. If you pass away while investing in the S&P 500 and your net assets in the U.S. exceed USD 60,000, your portfolio will be subject to an estate tax that can rise up to 40%.

These tax rules can significantly affect net investment returns and may require careful planning to manage effectively. Investors who are unaware of these implications may find that their actual returns are much lower than expected once taxes and administrative complexities are taken into account.

5. Currency Risk for NRIs

Currency fluctuations can significantly impact investment returns for NRIs. Since the S&P 500 is denominated in U.S. dollars, investors who earn or spend money in other currencies are exposed to exchange rate movements.

For example, if the U.S. dollar weakens relative to the investor’s home currency, the value of their investment may decrease even if the underlying stocks perform well. Currency volatility can therefore add an additional layer of risk that many investors overlook when focusing solely on market returns.

So What Next?

In summary, while the S&P 500 has long been seen as a simple and effective way to gain exposure to the U.S. stock market, it is not necessarily the optimal long-term strategy for NRIs seeking sustainable wealth creation and retirement planning. Concentration risks, limited global diversification, currency fluctuations, and complex tax implications can all reduce the effectiveness of relying solely on a U.S.-focused index.

A well-structured investment portfolio should instead prioritize broader diversification, professional management, and strategies that align with the unique financial and tax considerations of NRIs. This is where solutions like an Investment-Linked Policy (ILP) can play a role, offering access to globally diversified funds while combining long-term investment discipline with additional financial planning benefits.

Ultimately, the goal is not simply to invest in what is most popular, but to build a portfolio that is resilient, diversified, and aligned with your long-term financial goals. By looking beyond the traditional approach of investing solely in the S&P 500, NRIs can position themselves for more balanced growth and greater financial security in the years ahead.

If you would like to learn how you can leverage ILPs to create an investment portfolio that is better aligned to your goals, reach out to us today.