Why ILPs Are Excellent Tools for NRI Retirement Planning in Singapore

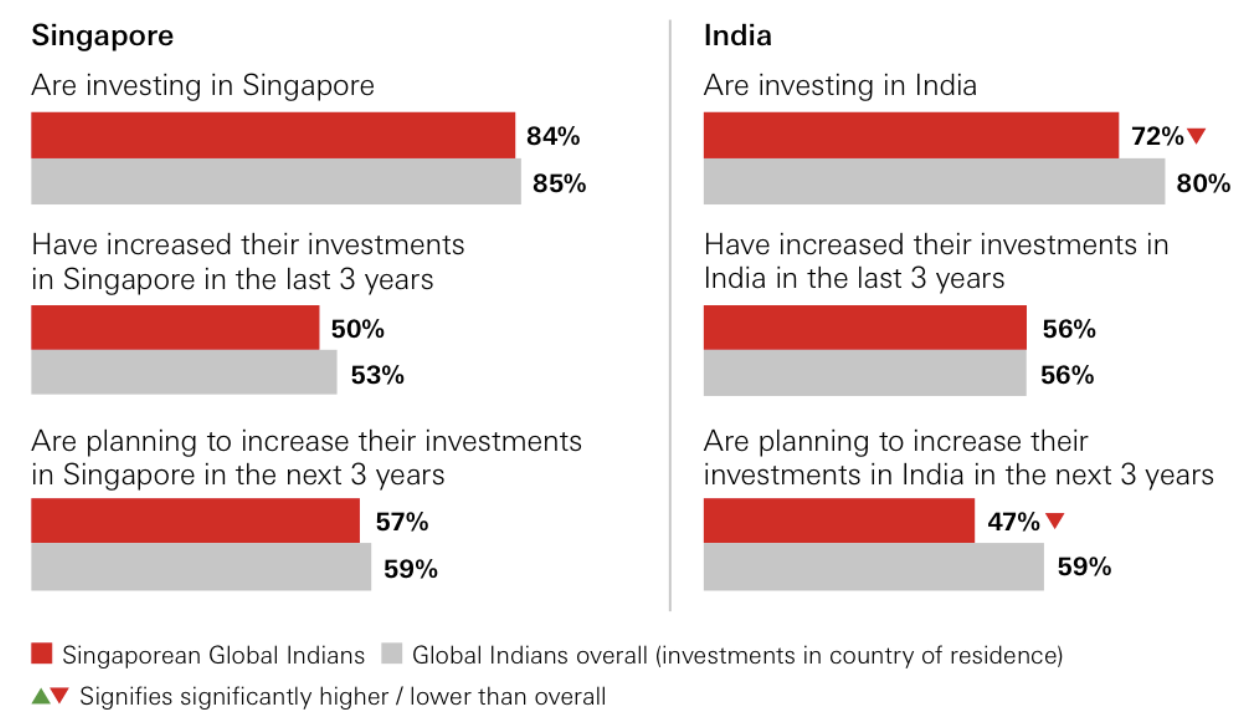

Singapore has long been a haven for investors due to its economic stature, political stability, and business-friendly regulatory environment. However, many NRIs also choose to have investments in India. This decision is often driven by a desire to maximize gains, invest in a familiar environment, and position their wealth in the country they prefer to retire in. According to research from HSBC, 85% of NRIs are currently holding some form of investments in Singapore and 80% simultaneously hold investments in India.

While most NRIs recognize that they should invest from their income in Singapore, it can be overwhelming with an increasing amount of options available for retail investors. Among these options are Investment-Linked Policies (ILPs) that are typically administered by large insurers. ILPs have evolved significantly in the past decade. This blog post will cover why NRIs should invest actively in Singapore and what role ILPs should play in their investment strategy.

Statistics from HSBC relating to Indians investing in Singapore and in India

Why Investments Are the Most Ideal Way You Can Reach Your Financial Goals

Many NRIs use a variety of strategies to build wealth and secure their retirement. Common choices include real estate investments, fixed deposits, or holding savings in bank accounts. While these options offer stability, they may not always generate the long-term growth necessary to meet retirement goals, especially in the face of inflation.

Investments that provide exposure to diversified financial markets such as equities, bonds, and global funds can potentially deliver stronger long-term returns. By consistently investing and allowing compounding to work over time, NRIs can gradually build a retirement corpus that supports their lifestyle after they stop working and even bring that retirement age down.

Additionally, investing through Singapore offers advantages such as access to global markets, strong regulatory protections, and a wide range of professionally managed funds.

What Is an ILP

There are many misconceptions about ILPs on the Internet and amongst people who might not have any recent interactions with advisors that truly understand the product. In the past, ILPs were structured like composite products that combined life insurance and investments in actively managed funds. This meant that part of your premium was redirected to pay for a term insurance plan baked into the ILP. The rest of your premium would then be invested. The implication of this was that your investments would have had to perform far above the benchmark in order for you to see any profits.

However, in response to feedback from clients and advisors, insurers in Singapore have stopped selling such products. ILPs today are purely investment tools. This means that every cent that you pay is invested directly into the funds that you and your advisor choose collaboratively. This dedicated investment structure is found commonly in Singapore now while ILPs in India still follow the traditional split approach.

How ILPs Help You Reach Your Retirement Goal

Now that you have a clearer understanding of how ILPs operate in Singapore in 2026, you can begin to explore how one can help you achieve your financial goals. Here are some benefits that you can expect to receive should you choose this tool to help you build the retirement of your dreams.

1. Actively Managed Funds

ILPs typically provide access to a curated selection of professionally managed funds. These funds are overseen by experienced fund managers who monitor markets, adjust portfolios, and seek opportunities across different asset classes.

For investors who may not have the time or expertise to manage their own portfolios actively, this structure allows them to benefit from professional investment management while still maintaining control over fund selection.

2. Access to Accredited Investor Funds

ILP platforms usually provide access to funds that are typically reserved for more sophisticated investors. These may include specialized strategies, private market exposure, or institutional-grade funds that are not easily available through standard retail investment platforms.

To qualify as an accredited investor in India, you need to have one of the following:

Annual income of INR 2 crore

Net worth of more than INR 7.5 crore with at least half in financial assets

In Singapore, you need to have one of the following:

Net personal assets of over SGD 2 million (primary residence value capped at SGD 1 million)

Minimum income of over SGD 300,000

When investing through ILPs, you are offered access to accredited investor funds without meeting the above qualifications. For NRIs seeking broader diversification, this access can open up opportunities that go beyond traditional equity and bond funds.

3. An Advisor That Is Answerable Only to You

A key advantage of working with an ILP structure is the ability to collaborate closely with a financial advisor. Instead of relying solely on automated tools or generic investment portfolios, you can receive personalized guidance tailored to your specific goals, risk tolerance, and retirement timeline.

This advisory relationship ensures that your investment strategy evolves alongside your life circumstances and financial objectives.

4. Fixed Fee Structure

Many modern ILP platforms operate with a transparent and predictable fee structure. Rather than relying on multiple layers of hidden costs, investors often benefit from clearly defined platform or advisory fees.

This transparency allows you to better understand how much you are paying for investment management and financial advice, making it easier to plan your long-term returns.

5. Increased Flexibility at No Cost

ILPs often allow investors to switch between funds as market conditions change or as personal financial goals evolve. For example, an investor may choose higher-growth equity funds during their early career and gradually transition to more conservative allocations as retirement approaches.

This flexibility helps ensure that your investment portfolio remains aligned with your risk tolerance and life stage without needing to completely restructure your investment plan.

If you would like to learn how you can start using our effective financial tools to achieve your financial goals, reach out to us today.